What are the main objectives of accounting and the rules of debit and credit?

Understand the Problem

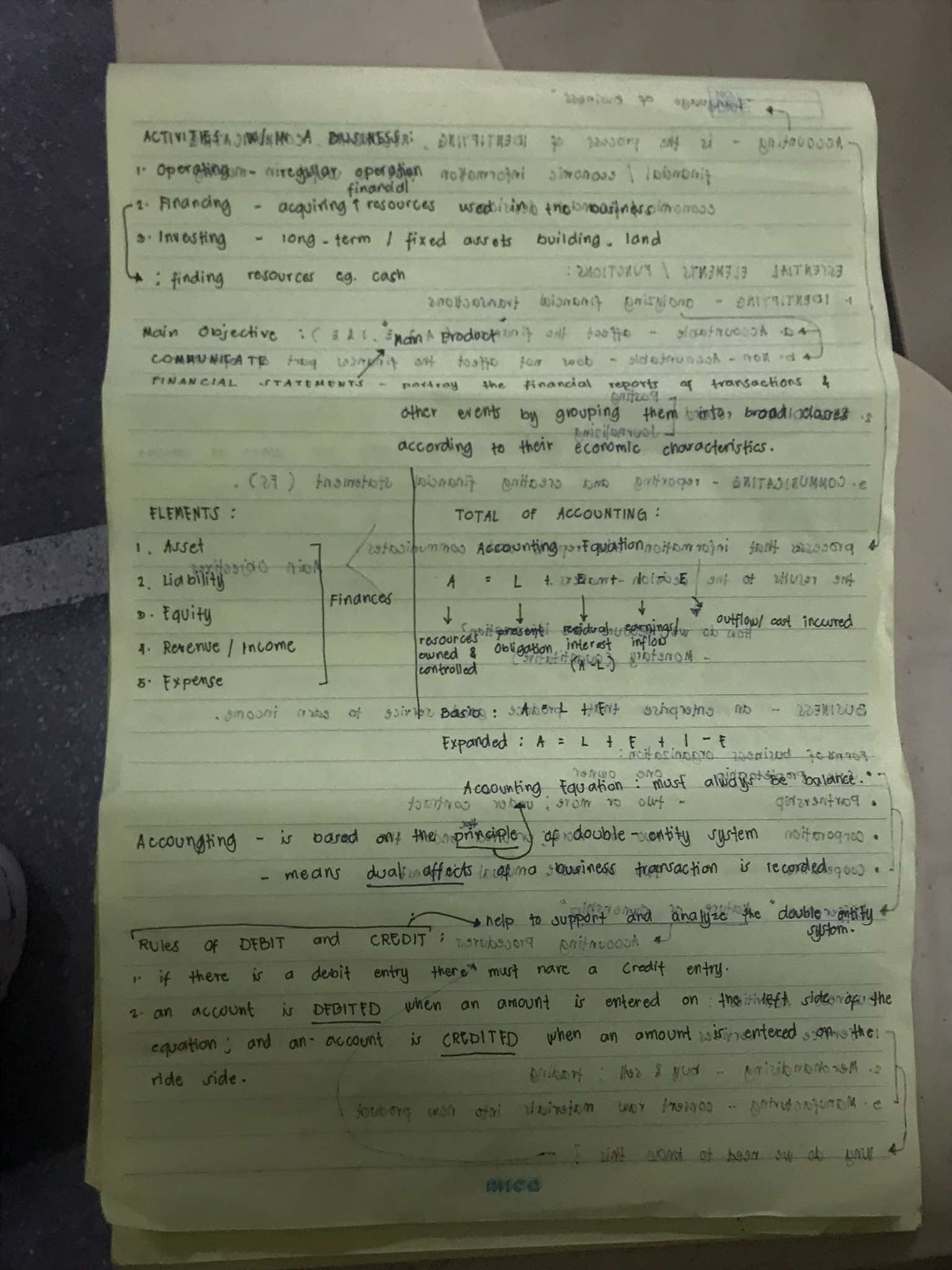

The question appears to cover various concepts related to accounting, including activities in a business, financial statements, and the principles of double-entry accounting. It outlines the main objectives of accounting and elements such as assets, liabilities, and equity. It also discusses the rules of debit and credit entries.

Answer

Accounting communicates financial info; debits increase assets and expenses, credits increase liabilities and revenue.

The main objective of accounting is to communicate financial information by preparing reports. Debits increase asset, expense, and loss accounts, while credits increase liability, equity, revenue, and gain accounts. Every debit entry must have a corresponding credit.

Answer for screen readers

The main objective of accounting is to communicate financial information by preparing reports. Debits increase asset, expense, and loss accounts, while credits increase liability, equity, revenue, and gain accounts. Every debit entry must have a corresponding credit.

More Information

Accounting aims to provide financial insights for decision-making. Debits and credits ensure transactions are accurately recorded, following the double-entry system.

Tips

Common mistakes include reversing debit and credit roles or forgetting the need for balance in entries.

Sources

- Debits and Credits Explained - Netsuite - netsuite.com

- Debits and Credits in Accounting | Overview - patriotsoftware.com

AI-generated content may contain errors. Please verify critical information