Podcast

Questions and Answers

What is a primary unacceptable form of identification when verifying a person's ID?

What is a primary unacceptable form of identification when verifying a person's ID?

- State-issued Driver's License

- Military ID

- Passport

- Social Security Card (correct)

Which of the following is a key technique for detecting fraud when verifying identification?

Which of the following is a key technique for detecting fraud when verifying identification?

- Checking for holograms on IDs

- Confirming the expiration date on IDs

- Asking for related identification documents

- Ensuring the ID photo matches the person (correct)

Which of the following is a red flag indicating the potential for fraud in identification?

Which of the following is a red flag indicating the potential for fraud in identification?

- Old passport with no damage

- State ID issued three years ago

- Temporary Driver’s License (correct)

- ID with a clear photo

Which evidence is prime for rejecting an identification during transactions?

Which evidence is prime for rejecting an identification during transactions?

When verifying ID, which of the following is NOT a technique recommended for ensuring validity?

When verifying ID, which of the following is NOT a technique recommended for ensuring validity?

What is required on a check endorsed by a Power of Attorney (POA)?

What is required on a check endorsed by a Power of Attorney (POA)?

When verifying signatures on a check, what should you compare the member's signature on the check to?

When verifying signatures on a check, what should you compare the member's signature on the check to?

What constitutes good standing for a member cashing a transit check?

What constitutes good standing for a member cashing a transit check?

What is a critical step in verifying a non-member's check?

What is a critical step in verifying a non-member's check?

What happens to a Power of Attorney (POA) authority upon the death of the principal?

What happens to a Power of Attorney (POA) authority upon the death of the principal?

In which scenario would it NOT be necessary to verify documentation of a Power of Attorney?

In which scenario would it NOT be necessary to verify documentation of a Power of Attorney?

What is the main feature that is often disputed in checks according to verification guidelines?

What is the main feature that is often disputed in checks according to verification guidelines?

What is the primary purpose of an endorsement on a check?

What is the primary purpose of an endorsement on a check?

Which of the following qualifies as a negotiable instrument requirement?

Which of the following qualifies as a negotiable instrument requirement?

What does 'stale-dated' mean in relation to checks?

What does 'stale-dated' mean in relation to checks?

What happens if the numerical and written amounts on a check differ?

What happens if the numerical and written amounts on a check differ?

Which of the following statements is true regarding checks made payable to 'Cash'?

Which of the following statements is true regarding checks made payable to 'Cash'?

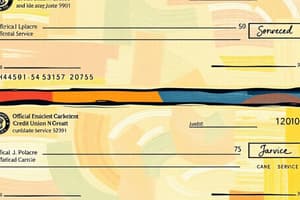

What is indicated by the MICR line on a check?

What is indicated by the MICR line on a check?

When are normal presentment times for checks generally set to expire?

When are normal presentment times for checks generally set to expire?

If a check is post-dated, what does it mean?

If a check is post-dated, what does it mean?

Which endorsement type is most commonly used for transferring a check to another party?

Which endorsement type is most commonly used for transferring a check to another party?

What must a check have in order to be considered valid under Article 3 of the Uniform Commercial Code?

What must a check have in order to be considered valid under Article 3 of the Uniform Commercial Code?

Flashcards

Power of Attorney (POA)

Power of Attorney (POA)

A legal document granting someone (POA) the authority to handle financial transactions for another person (principal).

Checking Endorsement by POA

Checking Endorsement by POA

A POA's signature on a check, explicitly stating their authority to handle the transaction for the principal.

Verifying Signatures

Verifying Signatures

Crucial step in handling checks to validate the authenticity of signatures, ensuring the correct payee.

Non-Member Cashing On-Us Check

Non-Member Cashing On-Us Check

Signup and view all the flashcards

Member Cashing Transit Check

Member Cashing Transit Check

Signup and view all the flashcards

Courtesy Pay (CP)

Courtesy Pay (CP)

Signup and view all the flashcards

Disputed Documents

Disputed Documents

Signup and view all the flashcards

Acceptable ID for Transactions?

Acceptable ID for Transactions?

Signup and view all the flashcards

Verification Red Flags

Verification Red Flags

Signup and view all the flashcards

Identity Theft Risk

Identity Theft Risk

Signup and view all the flashcards

What's Not an Acceptable ID?

What's Not an Acceptable ID?

Signup and view all the flashcards

Beyond Formal ID? Use Judgment!

Beyond Formal ID? Use Judgment!

Signup and view all the flashcards

Negotiable Instrument

Negotiable Instrument

Signup and view all the flashcards

Check Requirements (Article 3 UCC)

Check Requirements (Article 3 UCC)

Signup and view all the flashcards

Payable to a specific person/company

Payable to a specific person/company

Signup and view all the flashcards

Payable to "Cash" or "Bearer"

Payable to "Cash" or "Bearer"

Signup and view all the flashcards

Drawee

Drawee

Signup and view all the flashcards

Numerical Dollar Amount

Numerical Dollar Amount

Signup and view all the flashcards

Written Dollar Amount

Written Dollar Amount

Signup and view all the flashcards

Post-dated Check

Post-dated Check

Signup and view all the flashcards

Stale-dated Check

Stale-dated Check

Signup and view all the flashcards

Endorsement

Endorsement

Signup and view all the flashcards

Study Notes

Membership Eligibility

- Individuals can join Alliance Catholic Credit Union if they are:

- A relative of an existing member or immediate family member

- An employee of ACCU

- A student, faculty member, or alumnus of a Catholic University located in Michigan

- An employee or pensioner of a Catholic healthcare system located in Michigan

- A resident, employee, student, or person of Catholic faith who attends, works, or worships within the state of Michigan

- A retiree living in Genesee, Lapeer, Livingston, Monroe, St. Clair, Wayne, Oakland, Macomb, or Washtenaw counties

- A member of a select employee group (SEG) affiliated with ACCU or a member of parishes, schools, or organizations associated with Catholic churches in Michigan

- A resident, worker, student, or worshiper of the Texas counties comprising the Diocese of Tyler or the Diocese of Austin, Texas

Mission Statement

- A mission statement defines an organization's purpose and reason for existing

- A mission statement guides the actions of an organization

- The goal is to provide trusted financial services inspired by Catholic values and traditions to enhance the financial wellbeing of communities and neighbors.

Vision Statement

- A vision statement describes an organization's aspirations and future goals

- Vision statements help guide individuals in their tasks

- A vision statement should help guide individuals in the next 5–10 years

- The vision of Alliance Catholic Credit Union is to become the nation's primary provider of innovative financial solutions for Catholics and their neighbors, delivered with personalized and trusted service.

Member Service Skills

- First impressions are crucial

- Making a positive first impression is essential

- Basic member skills are foundational interactions

- Important skills include greeting people, developing rapport, listening carefully, being tactful, and saying thank you.

Negotiable Instruments

- Negotiable instruments are financial documents that can be converted to cash upon demand

- Examples are paper money, checks, bonds, etc

- Currency denominations commonly used are 1,1, 1,5, 10,10, 10,20, 50,and50, and 50,and100

- Currency paper is made of 25% linen and 75% cotton with red and blue synthetic fibers spread evenly

- Watermarks are added to help prevent fraud on currency (1996 series and higher)

Negotiable Instruments - Overview of a Draft/Check

- Key elements of a check include the maker, date, check number, payee, numerical and written dollar amounts, drawee, memo line, signature, and MICR line.

Negotiable Instruments

- An instrument must contain words of negotiability, such as “Pay to the Order of”

- The instrument must be payable to a specific person, company, or “bearer“(Cash)’

- To be negotiable, it must be payable to a specific organization or specific person

- If payable to "cash" or "bearer" it is negotiable to anyone

- For a check to be negotiable, it must have a drawee (bank or credit union) authorized to pay it

Negotiable Instruments - Payment

- The written amount is the legal amount if the written and numerical amounts differ

- The instrument must contain a fixed date

- Usual timeframe for presentment is 6 months from the date on the check.

- Postdated checks are not negotiable until the date on the check

- Stale-dated checks (past date) may have exceptions that are on the check; usually government checks are negotiable for 12 months, some checks may have an expiry date of 90 days.

Endorsements

- Endorsement of a check is a signature or stamp by the payee, to indicate that it has been transferred

- The endorsement acts to guarantee the item and acknowledges receipt of funds (check).

- Special circumstances may require another person to endorse a check on behalf of a payee

- The documentation includes a birth certificate, and official guardianship documents.

Endorsements - Payable to a Minor

- The appropriate endorsement for a check made payable to a minor (too young to endorse themselves) includes writing, the child's name, “A Minor” then signing the parent/legal guardian.

Endorsements - Payable to a Person with a Representative Payee

- Representative payees (selected individuals or agencies/organizations) manage funds for persons unable to manage themselves (incapacitated).

- Representative payee needs account before check negotiation.

- Common examples of those who require a payee include minors and legally incompetent adults.

Endorsements - Payable to an Individual, but "Power of Attorney"

- A Power of Attorney (POA) is granted by a person ("principal") to another person to handle financial transactions on their behalf.

- POA can endorse checks by printing the principal's name on the first line and POA's signature followed by "POA" on the second line

- Verification of POA's authority is necessary and should be documented

Verifying Signatures

- Validating signatures on checks is crucial in legal and criminal matters, as handwriting is most important

- A member's signature must match the one in the file

- The name on the check should match the ID provided

- The non-member's signature should match the signature on their ID

Red Flags During Signature Verification

- Look out for overwriting, erasures or correction fluid, different inks, uneven pressure, pen-lifts, tremor, ink blots, smudges, or misspellings

- Contact a supervisor if you have any doubt.

Identification

- Verify the person's identity. Identify any fraud when a newly issued identification is presented.

- The date on the identification must match the person's age approximately.

- Discretion must be used when reviewing identification.

- Unacceptable forms of primary identification include Social Security Cards, birth or marriage certificates, library cards, armed forces discharge cards, and non-photo IDs

Robbery Awareness

- Awareness of robbery risk in the workplaces is necessary to keep employees aware

- Robberies commonly take place between 9:00 AM and 11:00 AM on Fridays.

- Types of robberies include, demand note robberies, verbal demand robberies, and take over robberies

- Statistically, robbers are often Caucasian, male, alone, and amateurs, with gains under $10,000

Studying That Suits You

Use AI to generate personalized quizzes and flashcards to suit your learning preferences.

Related Documents

Description

Test your knowledge about the membership eligibility criteria for Alliance Catholic Credit Union. This quiz covers various groups who can join based on their relationships, employment, or affiliations. Understand who can take advantage of ACCU's services and benefits.